Making Your Charity Eligible for Tax-Deductible Donations

If you’re running a not-for-profit in Australia, getting endorsed by the Australian Taxation Office (ATO) is a crucial step. This endorsement is what grants you Deductible Gift Recipient (DGR) status, and it’s a game-changer for your fundraising efforts. Simply put, it means your supporters can claim tax deductions on their donations, making it much more attractive for them to contribute to your cause.

This guide is designed for the people on the ground the dedicated founders, board members, and treasurers of Australian charities and community groups. Whether you’re running a cultural body, a local temple, an environmental group, or an educational institution, understanding how to apply for DGR status is essential for unlocking your organisation’s full potential.

What Is DGR Status?

Deductible Gift Recipient (DGR) status is a formal endorsement from the Australian Taxation Office (ATO) that allows an organisation to receive gifts and donations that are tax-deductible for the donor. When an individual or business donates $2 or more to a DGR-endorsed charity, they can claim that amount as a deduction on their tax return.

This status is regulated by both the ATO and the Australian Charities and Not-for-profits Commission (ACNC), who work together to ensure that organisations with DGR status meet and maintain strict governance and reporting standards.

The benefits of securing DGR endorsement are significant:

- Boosted Donations: The promise of a tax deduction is a powerful motivator for both individual donors and corporate sponsors.

- Increased Donor Trust: DGR status acts as a government-backed seal of approval, signalling that your organisation is a legitimate and well-governed charity.

- Access to More Funding: Many philanthropic foundations and government grant programs list DGR endorsement as a mandatory eligibility requirement.

Eligibility Requirements for DGR

Before you begin the application process, it’s vital to confirm your organisation meets the core eligibility criteria. A thorough self-check at this stage can save you from investing time and resources into an application that is destined for rejection.

The key requirements are:

- Must be a not-for-profit (NFP) entity: Your organisation’s governing documents must clearly state that it operates not for the profit or gain of its individual members.

- Must fall under a specific DGR category: Your organisation’s primary purpose and activities must align with one of the DGR categories defined in Australian tax law. Simply doing ‘good work’ is not enough; you must fit into a legislated category.

- Must have a suitable governing document: Your constitution, trust deed, or rules of association must contain specific clauses, particularly regarding its not-for-profit nature and how assets will be handled if the organisation winds up.

- Must be registered with the ACNC: For the vast majority of organisations seeking DGR endorsement, being registered as a charity with the ACNC is a prerequisite.

It’s a surprising fact, but even though there are over 60,000 registered charities in Australia, roughly half are ineligible for DGR status because their purpose doesn’t match a legislated category. This is a point of ongoing debate, and you can read more about the call for DGR reform on Community Directors.

Different Types of DGR Categories

When you apply for DGR status, one of the most critical steps is identifying the correct DGR category for your organisation. This determines whether your entire organisation can be endorsed, or only a specific part of it, such as a fund, authority, or institution it operates.

For example, a Public Benevolent Institution (PBI) is generally endorsed as a whole entity. In contrast, an organisation might operate a specific school building fund, where only donations made to that particular fund are tax-deductible.

To find your fit, your best resource is the DGR table provided by the ATO. You must find the category that genuinely reflects your organisation’s day-to-day purpose and activities.

Some common DGR categories include:

| DGR Category | Examples of Organisation Types | Key Purpose |

|---|---|---|

| Public Benevolent Institution (PBI) | Homeless shelters, disability support services | Directly relieving poverty, sickness, or distress. |

| Health Promotion Charity | Public health awareness groups, medical research foundations | Promoting the prevention or control of diseases in humans. |

| School Building Fund | Schools or community groups raising funds for school construction | Operating a fund solely for acquiring, constructing, or maintaining a school building. |

| Animal Welfare Charity | Animal rescue groups and shelters | Providing short-term care and rehoming for abandoned or mistreated domestic animals. |

| Cultural Organisation | Galleries, museums, performing arts companies | Must be on the Register of Cultural Organisations to promote arts and culture. |

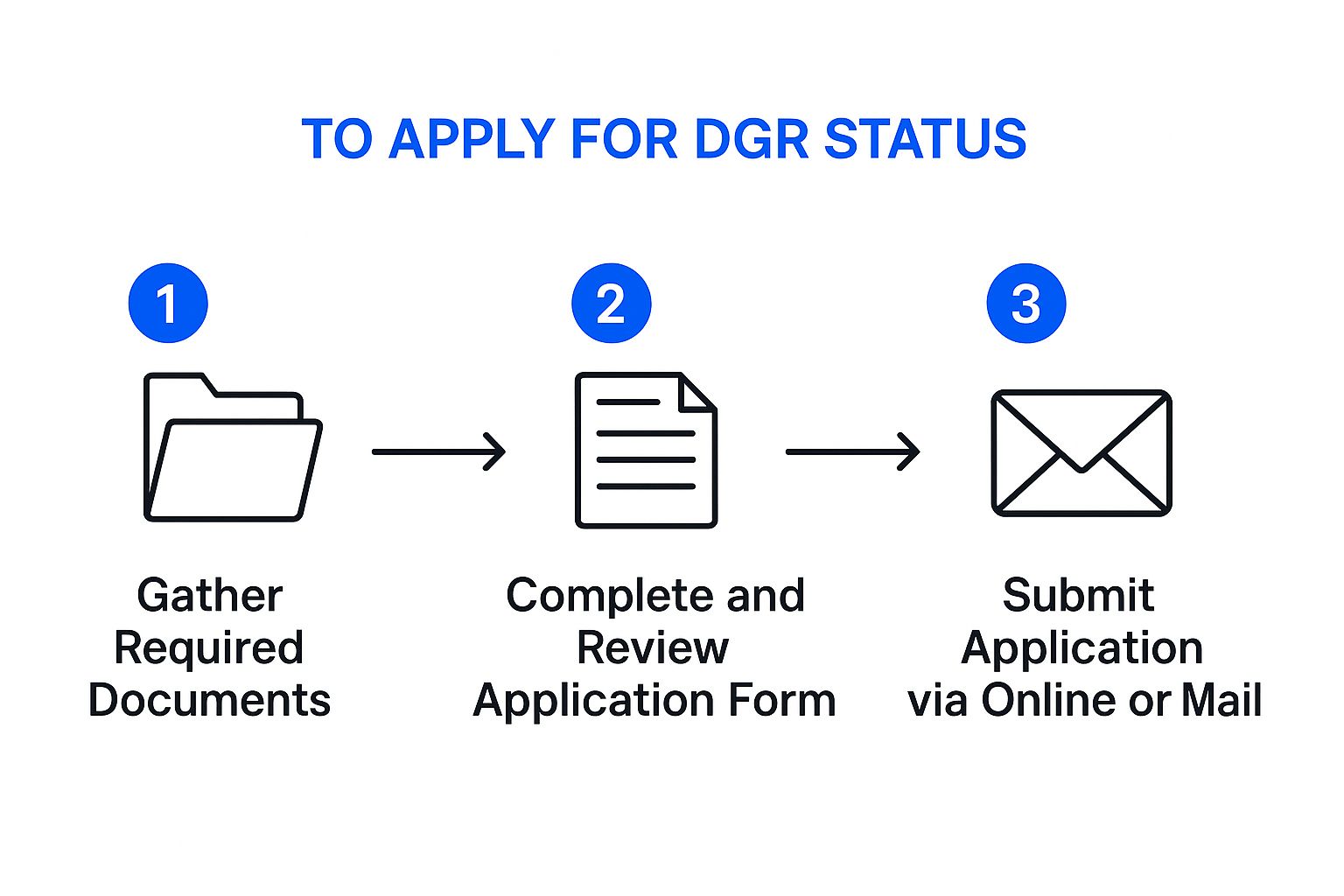

How to Apply for DGR Status: Step-by-Step

Once you’ve confirmed your eligibility and identified the right category, you can move on to the application itself. The process requires careful attention to detail.

1. Register as a Charity with the ACNC

For most organisations, the first step is to become a registered charity with the Australian Charities and Not-for-profits Commission (ACNC). This is a non-negotiable prerequisite.

2. Identify the Relevant DGR Category

Using the ATO’s DGR table, pinpoint the exact category that matches your organisation’s purpose and activities. This choice will guide the rest of your application.

3. Update Your Governing Documents

Review your constitution or rules to ensure it contains the specific clauses required by the ATO. This includes appropriate DGR winding-up and gift fund clauses. Using the ATO’s recommended wording is highly advised to avoid compliance issues.

4. Prepare Supporting Documentation

Gather the evidence that proves your organisation’s charitable work. This can include:

- A detailed statement of purpose and activities.

- Financial statements.

- Annual reports, program flyers, or website content that demonstrates your activities.

5. Submit the Application

For most charities, the DGR application is part of the charity registration process via the ACNC Charity Portal. In other cases, you may need to apply directly to the ATO via the Australian Business Register (ABR).

6. Wait for Assessment and Respond to Requests

After submission, the ATO will assess your application. It is common for them to request further information. Respond to any requests promptly and thoroughly to keep the process moving.

7. Receive Outcome

You will receive a notice of decision. If successful, your DGR endorsement will be active from the date specified in your approval.

Common Reasons for Rejection

A rejected application can be a major setback. Most rejections are due to a few common and avoidable mistakes:

- Constitution missing required clauses: Your governing document must contain the ATO’s mandatory winding-up and gift fund clauses, often word-for-word.

- Applying under the wrong DGR category: Your stated activities must perfectly align with the category you’ve selected.

- Not demonstrating the charitable purpose clearly: Vague statements like “supporting the community” are not enough. You must provide concrete evidence of your work.

- Applying without being ACNC-registered (where required): For most applicants, ACNC charity registration is a mandatory first step.

Ongoing Obligations After Receiving DGR Status

Securing DGR endorsement is not a one-off task; it comes with ongoing responsibilities to maintain public trust and regulatory compliance.

Your key obligations include:

- Continuing to operate as a not-for-profit: All funds must be used to pursue your endorsed charitable purpose.

- Using funds correctly: Donations received for your DGR purpose must only be used for that purpose.

- Updating your details: You must notify the ACNC and update the Australian Business Register (ABR) of any changes to your organisation’s name, address, or responsible persons.

- Lodging annual statements: You must submit an Annual Information Statement to the ACNC each year, along with financial reports if required.

- Notifying the ATO of major changes: If you amend your constitution or your core purpose changes, you must inform the Australian Taxation Office (ATO) as this could affect your eligibility.

How Nanak Accountants & Associates Can Help

The path to apply for DGR status can feel like a maze, but you don’t have to walk it alone. At Nanak Accountants & Associates, we have successfully guided countless not-for-profits including community organisations, temples, educational institutions, and cultural bodies through this exact process.

We can help with:

- Selecting the correct DGR category.

- Reviewing and updating your governing documents.

- Preparing and lodging a complete and compliant application.

- Ensuring ongoing compliance with ATO and ACNC requirements.

We specialise in building robust, compliant applications that stand the best possible chance of success. Contact us today to get started.

")